What Every Family Needs to Know — Without the Jargon

Based on the FTA’s updated Corporate Tax Guide on Taxation of Family Foundations (CTGFF1), June 2026

If you’ve built wealth in the UAE — properties, share portfolios, stakes in businesses you want your children and grandchildren to inherit smoothly — chances are someone has already told you to “set up a foundation.” And if you’ve started looking into it, you’ve probably run into a wall of terms: fiscal transparency, unincorporated partnership, Article 17, multi-tier structures. It can feel like you need a law degree just to protect what you’ve already earned.

The good news is that the underlying idea is actually simple, and the Federal Tax Authority’s freshly updated guide (June 2026) makes the rules clearer than they’ve ever been. Let me walk you through the whole thing the way I would explain it to a friend over coffee — with pictures, real examples, and none of the legalese.

First things first: what is a “Family Foundation”?

Here’s something that surprises almost everyone. A Family Foundation is not a type of company you register somewhere. You won’t find a counter at DIFC or ADGM with a sign saying “Family Foundations — apply here.”

It’s a tax status, not a legal entity.

The Corporate Tax Law uses the term for any foundation, trust, or similar structure that a family uses to hold and manage its wealth — and that meets a specific set of conditions. The underlying vehicle could be a DIFC foundation, an ADGM foundation, a RAK ICC foundation, a trust under the Federal Trust Law, or even a foundation set up outside the UAE entirely. The legal wrapper is one question; the tax status is another. What matters for tax is whether the structure ticks the right boxes.

One more piece of housekeeping before we go further. Structures come in two flavours:

- Incorporated structures (most foundations, and trusts registered under the Federal Trust Law) have their own legal personality. By default, the tax system treats them like companies — they would pay Corporate Tax on their own income unless they apply for special treatment.

- Unincorporated structures (like contractual DIFC or ADGM trusts) have no separate legal personality. They are automatically “looked through” for tax — no application needed — though qualifying as a Family Foundation still matters for the companies sitting underneath them, as we’ll see.

Why does anyone want this status? One word: transparency

And no, not the corporate-governance kind.

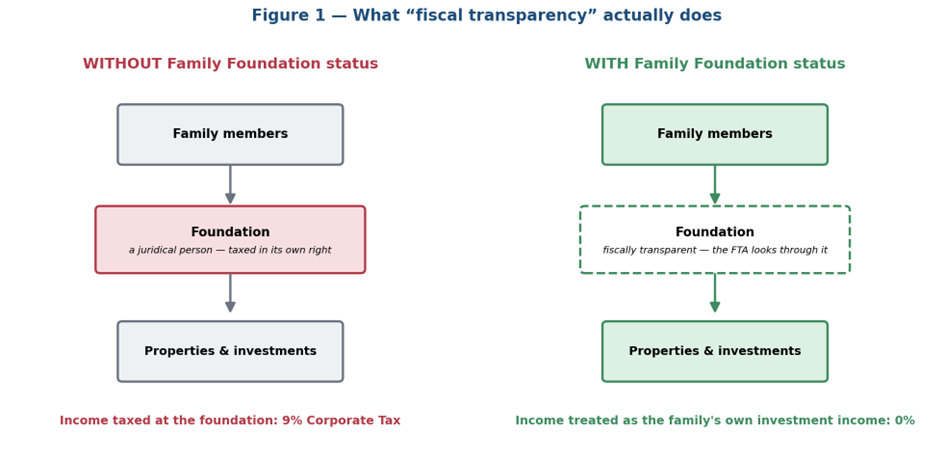

Normally, if your foundation is a juridical person — meaning it has its own legal personality, separate from you — the taxman treats it like any other company. Its profits could face 9% Corporate Tax.

But here’s the thing. If you, as an individual, held those very same assets directly — your rental apartments, your share portfolio, your bond holdings — most of that income wouldn’t be taxed at all. The UAE deliberately keeps individuals out of Corporate Tax for three categories of income: Wages, Personal Investment income (investments held for your own account, not through a licensed business), and Real Estate Investment income (buying, selling and renting property without needing a commercial licence).

So a strange unfairness would arise: put your assets in a foundation for perfectly sensible succession reasons, and suddenly the same income becomes taxable. The law fixes this. A foundation that qualifies as a Family Foundation can apply to the FTA to be treated as “fiscally transparent” — technically, as an “Unincorporated Partnership.” In plain English: the tax authority looks straight through the foundation as if it weren’t there, and treats the income as belonging directly to the beneficiaries, usually the family members.

The result, as Figure 1 shows, is that the family ends up in exactly the same tax position as if they had never put the assets into a foundation at all. The structure gives you succession planning, asset protection and governance — without creating a tax bill that wouldn’t otherwise exist. That is the entire point of the regime.

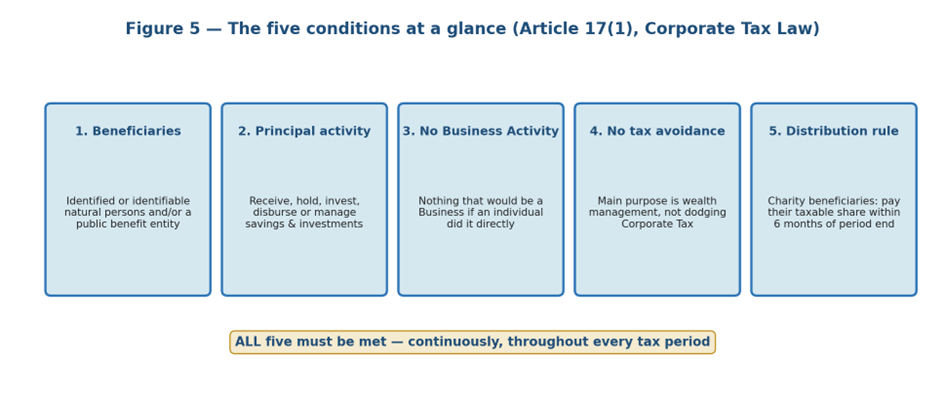

The five conditions — the heart of the whole thing

To qualify under Article 17(1) of the Corporate Tax Law, your foundation or trust has to meet all five of the following conditions — not most of them, all of them, and continuously throughout the tax period.

1. The beneficiary test

The foundation must exist for the benefit of identified or identifiable natural persons, a public benefit entity (think charities and not-for-profits), or both. “Identifiable” is generous here — your future grandchildren, not yet born, still count as long as they’re described as a class of beneficiaries (“the children and grandchildren of the founder”). Two more things people find surprising: there is no minimum or maximum number of beneficiaries, and the beneficiaries don’t even have to be from the same family. Two business partners could, in principle, share one qualifying structure.

2. The principal activity test

The foundation’s main job must be to receive, hold, invest, disburse or otherwise manage assets and funds associated with savings or investment. Buying and selling shares, bonds and property to grow the pot or generate income for the family — all fine. Distributing money to beneficiaries, funding charitable causes, paying an investment manager or a family office for its services — also fine. This condition is rarely the problem.

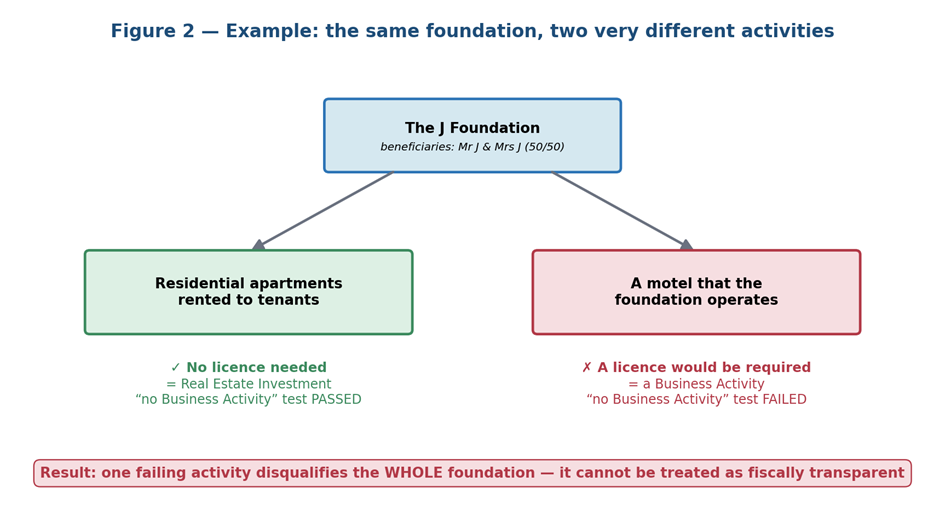

3. The “no business” test — the one that trips people up

The foundation must not do anything that would count as a Business or Business Activity if an ordinary individual did it directly. The logic ties back to those individual exemptions we mentioned: the foundation can do whatever you could do tax-free as a person — personal investing and unlicensed real estate investment — but it cannot run what is effectively a commercial operation.

The FTA’s own example makes this beautifully concrete. Picture the J Foundation, whose beneficiaries are Mr J and Mrs J, holding two kinds of property:

Renting out residential apartments needs no licence — if Mr and Mrs J did it themselves it would be Real Estate Investment income, so the foundation doing it is fine. But operating a motel would require a licence; done by an individual it would be a Business. And here’s the sting in the tail: it isn’t just the motel income that becomes taxable — the entire foundation fails the conditions and cannot be treated as transparent at all. One commercial activity poisons the whole well. If your structure mixes passive holdings with anything operational — a hotel, a managed serviced-apartment business, a trading activity — that operational piece needs to live somewhere else.

4. The no-tax-avoidance test

The main or principal purpose of the foundation can’t be dodging Corporate Tax. That sentence makes some clients nervous, but the guide is explicitly reassuring: simply applying for transparent treatment, and thereby ending up with income outside the tax net, is not in itself avoidance. Using the structure for what it’s designed for — holding, investing and passing on family wealth — satisfies this condition. It only bites where a structure is contrived for a tax outcome rather than a genuine wealth-management purpose.

5. The distribution test (only when a charity is a beneficiary)

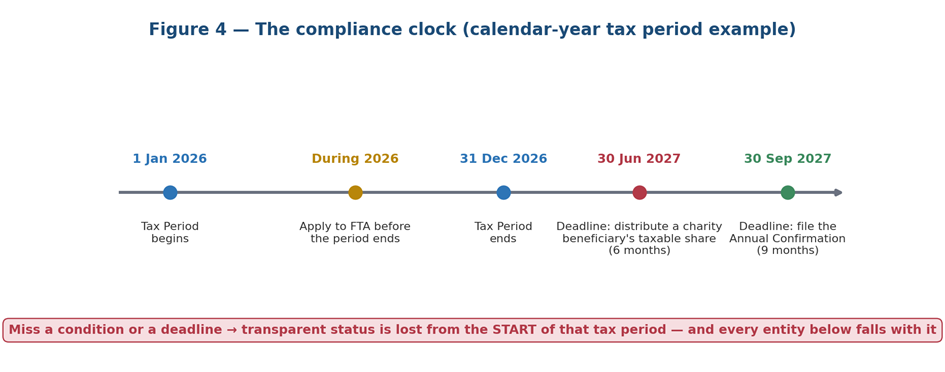

Many families name a charitable organisation alongside the children. If you do, there’s one extra rule. Either the charity’s share of the income must be the kind that wouldn’t have been taxable in its hands anyway (for example, UAE dividends, or income covered by the Participation Exemption, or the charity is a Qualifying Public Benefit Entity that’s exempt altogether) — or the foundation must actually pay out the charity’s share of taxable income within six months of the end of the tax period.

A worked example from the guide: a foundation buys 10% of a foreign company in February and sells most of it in October at a gain. Because the shares weren’t held for twelve months, the Participation Exemption doesn’t apply — so the charity’s slice of that gain is the taxable kind. For a December year-end, the foundation must pay the charity its share by 30 June of the following year. Miss that deadline, and the foundation — and every company under it — loses its transparent status retroactively, from the start of that tax period. Note the asymmetry: there is no obligation to distribute the family members’ share. The deadline only exists for the charity.

What about the companies under the foundation?

This is where the June 2026 guide really earns its keep, because real-world family structures are rarely a single foundation holding assets directly. The typical setup is a foundation at the top, with one or more SPVs or LLCs underneath — one holding the Dubai properties, another holding the listed portfolio, perhaps a third holding an overseas investment.

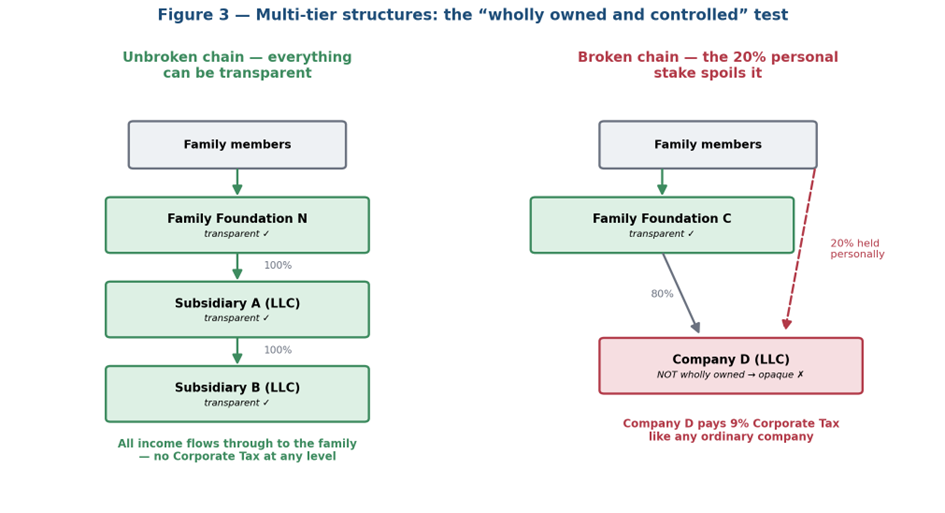

An LLC, on its own, can never be a “similar entity” to a foundation or trust — a commercial company doesn’t qualify by itself. But the law provides a second door: a juridical person that is wholly owned and controlled by a Family Foundation can also apply to be treated as fiscally transparent, provided two things are true:

- The ownership and control run through an unbroken chain — either directly, or through intermediate entities that are themselves all fiscally transparent, and

- The company itself meets the same Article 17(1) conditions (so no commercial activities inside the SPV either).

The word “unbroken” matters enormously, and Figure 3 shows why. On the left, Family Foundation N wholly owns Subsidiary A, which wholly owns Subsidiary B; both subsidiaries only hold family real estate. Every link is intact, every entity can be transparent, and the rental income flows through to the family as untaxed Real Estate Investment income.

On the right is the cautionary tale. Family Foundation C owns 80% of Company D — but one family member personally holds the other 20%. Company D is no longer wholly owned by the foundation. The chain snaps at that point: Company D is opaque and pays Corporate Tax like any normal business, and anything Company D itself owns is dragged down with it. (The family member’s own dividends from Company D can still be untaxed Personal Investment income in their hands — but the company-level tax is now real.)

A few practical confirmations in the new guide that advisors have been waiting for:

- A company can be wholly owned jointly by two or more Family Foundations and still qualify — useful where two branches of a family each have their own foundation but co-invest through one SPV.

- Entities in the chain don’t need the same financial year — but watch the overlap. For a subsidiary with a March year-end to be transparent, its parent must be transparent for the subsidiary’s entire tax period, which can span two of the parent’s periods.

- For unincorporated trusts, it doesn’t matter that legal title sits with the trustee. The trustee holding bare legal title isn’t taxed on the trust assets or their income — only on its own trustee fees.

- When a company moves in or out of a foundation’s ownership, there is no reset of the base cost of its assets — the transparent years are simply ignored for that purpose.

A word on foreign foundations

There’s no requirement for the structure to be a UAE entity, and for many GCC families this is the headline. Take a family resident in another Gulf country that sets up a foundation at home to hold its Dubai rental apartments. Because the foundation earns income from UAE immovable property, it has a “nexus” here — it must register for Corporate Tax and would, by default, be taxed as a non-resident on the rental profits.

But if it meets all five conditions, that foreign foundation can apply for Family Foundation treatment exactly like a UAE one. If approved, the FTA looks through it; the rent is treated as the family members’ own Real Estate Investment income; and nobody pays Corporate Tax on it — even though the family lives abroad and the foundation was formed abroad. The foundation should simply be ready to show the FTA documents from its home jurisdiction proving it really is a foundation or trust and that its beneficiaries qualify.

One caveat from the guide’s own example: if a beneficiary of that foreign structure is a foreign charity, the look-through can drag the charity itself into UAE Corporate Tax on its share of the UAE property income — because it now has a nexus here too. Worth checking before you finalise the beneficiary list.

The family office is a different animal

Plenty of wealthy families also run a family office — a company that manages the investments, handles the reporting, employs the staff. Can that be transparent too?

Almost certainly not, and the guide is refreshingly blunt about it. A single or multi family office provides services for fees — that is a Business Activity, which fails condition three. The family office pays Corporate Tax on its income like any other company, and it must charge the family arm’s-length fees for its services, because the family members and the foundation are related parties.

There is a silver lining: if the family office sits in a free zone and its wealth or investment management services are under the regulatory oversight of a competent authority (the DFSA in DIFC, the FSRA in ADGM, or the UAE Central Bank), those services can be Qualifying Activities eligible for the 0% free zone rate. But note the fine print — merely holding a licence isn’t enough; actual regulatory oversight is required. That’s a separate analysis from the Family Foundation regime, and the two shouldn’t be confused.

Putting assets in: a quick word on transfers

When the founder transfers assets into the foundation — at setup or later — the founder and the foundation are typically Related Parties, so the transfer should happen at arm’s-length values. For most founders this is a non-event: where the transferor is an individual and the assets are personal investments or unlicensed real estate, the transfer simply isn’t subject to Corporate Tax. But if assets are coming out of a taxable company into the foundation, the gain or loss on that transfer can have tax consequences, so sequence the funding carefully.

The paperwork you can’t skip

The regime is generous, but it is not automatic, and it is not “set and forget.” Three dates deserve a permanent place in your calendar.

- Register first. Every juridical person in the structure — the foundation and each company under it — needs its own Corporate Tax registration (its own TRN) before it can apply for transparent treatment. Even unincorporated trusts that are transparent by default must register.

- Apply before the tax period ends. The application must reach the FTA before the end of the period you want it to cover, and it can take effect from the current period or the next one. In a multi-tier structure, the foundation can submit one application on behalf of all the underlying entities (each entity authorises it) — which saves real administrative pain.

- File the Annual Confirmation. This is the one people forget. Once approved, you must confirm to the FTA — every single year, within nine months of the period end — that you still meet all the conditions. Again, the top entity can file one confirmation covering the whole structure.

And if you stop meeting the conditions mid-year? The status doesn’t end from that date — it’s lost from the beginning of that tax period, and every entity below the failing one falls with it. A foundation that quietly started a commercial activity in November could find its entire year’s income — and its subsidiaries’ income — retroactively taxable. Hardly a gentle landing, which is why ongoing monitoring matters at least as much as the initial setup.

The bottom line

The Family Foundation regime is genuinely one of the more family-friendly features of UAE Corporate Tax. It lets you wrap proper governance, asset protection and succession planning around your wealth without paying a tax price for doing so — the FTA simply pretends the wrapper isn’t there.

But it’s conditional, it’s annual, and the conditions interact in ways that aren’t obvious from a first read. One motel, one 20% personal shareholding in the wrong place, one missed six-month distribution to a charity, or one forgotten annual confirmation can unwind the entire structure — retroactively.

If you’re thinking about setting up a structure, or you already have one and the words “annual confirmation” made you slightly uneasy just now, it’s worth a proper review rather than a guess.

This article is a general summary of FTA Corporate Tax Guide CTGFF1 (June 2026) and does not constitute tax or legal advice. The guide itself is not legally binding, and every family’s structure is different — speak to a qualified UAE tax advisor about your specific circumstances.